When2Buy · Option POD3

0DTE Iron Condor Real-Price Backtest

Diagnostic backtest using historical Alpaca option bars for SPY + QQQ 0DTE iron condors. This page is intentionally blunt: the current real-price backtest is not launch-ready; it exposes sizing / payoff-model risk that synthetic tests hid.

Generated 2026-05-13 03:27 UTCPeriod 2024-02-01 → 2026-05-11Real option bars, no synthetic fallback

Full trades

1,119

Full win rate

85.7%

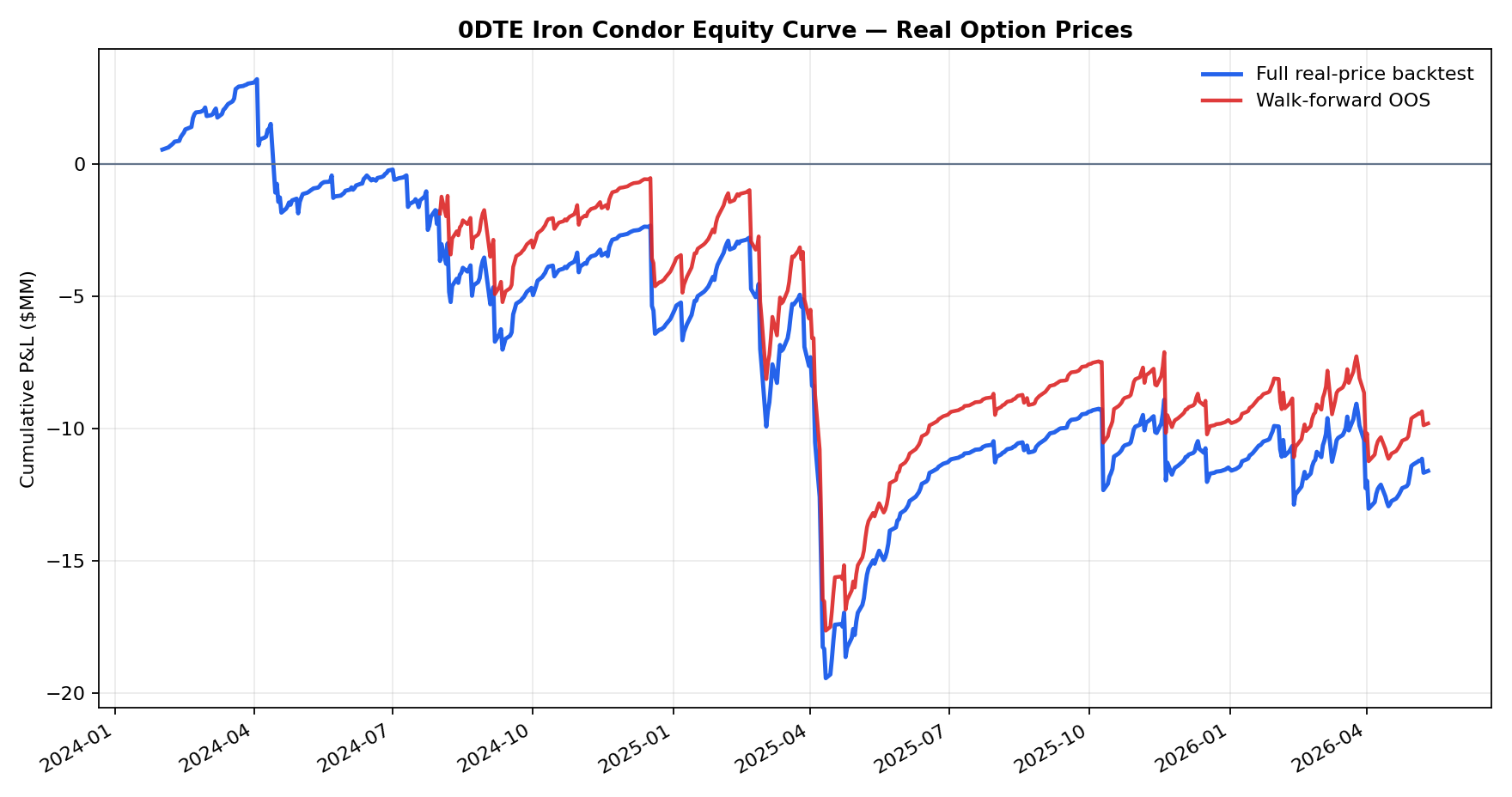

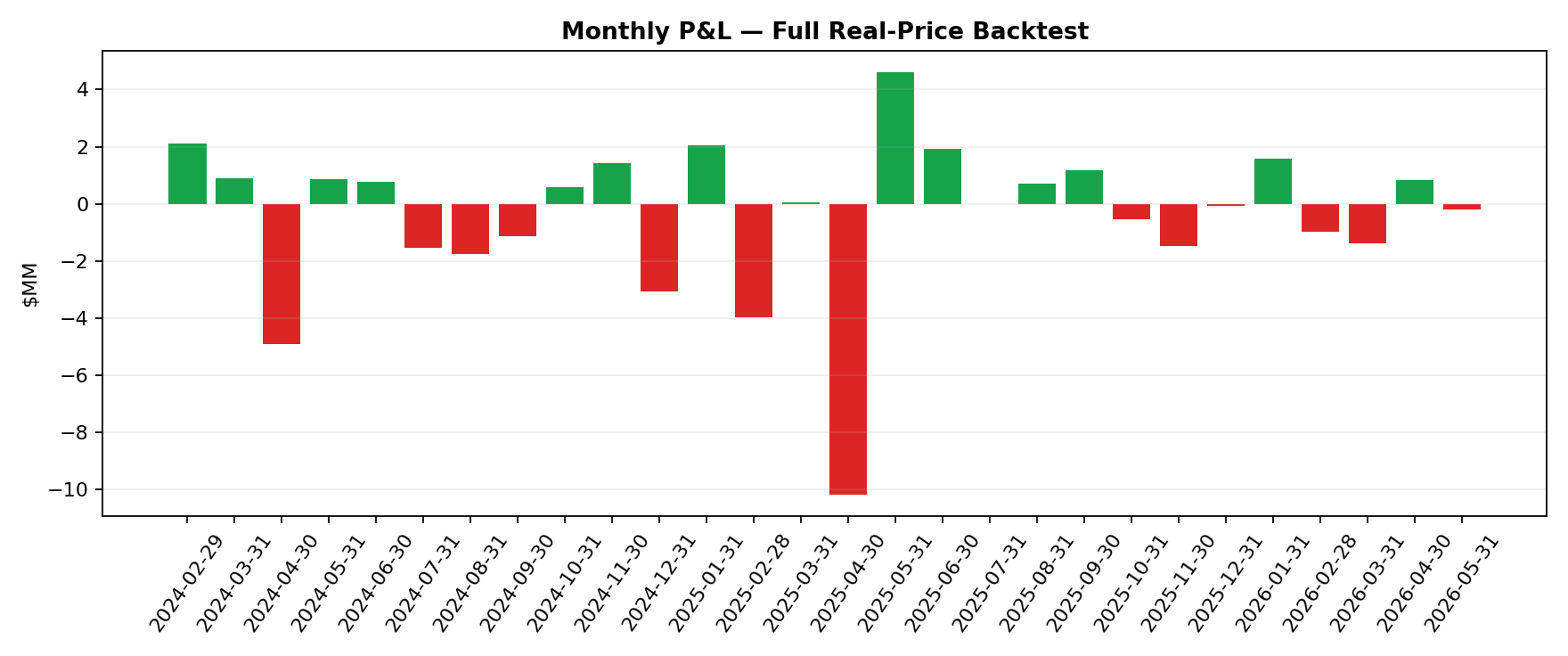

Full total P&L

-$11.61M

Full Sharpe

-0.62

OOS trades

874

OOS win rate

84.7%

OOS total P&L

-$9.82M

OOS max drawdown

-$17.11M

Equity curve

Monthly P&L

Original backtest figure

What was tested

- Underlying universe: SPY + QQQ

- Structure: 0DTE iron condor

- Pricing source: Alpaca historical option bars

- Entry/exit: conservative bid/ask real-price replay

- Fallbacks: no synthetic option-price fallback for missing data

- Transformer unavailable in this environment; run used HMM/calendar path only, with HMM dependency missing so regimes collapsed to bull-only.

Next fixes before production

- Normalize P&L by real defined risk / contract count.

- Add final expiry settlement reconciliation.

- Restore HMM + transformer dependencies for regime filtering.

- Add mega-cap earnings / NVDA spillover filter.

- Re-run OOS after correcting payoff scaling.

Walk-forward folds

| Fold | Period | Trades | Win rate | P&L |

|---|---|---|---|---|

| F1 | 2024-08-01 → 2024-09-30 | 84 | 81.0% | -$2.90M |

| F2 | 2024-10-01 → 2024-11-29 | 86 | 89.5% | $2.00M |

| F3 | 2024-12-02 → 2025-01-31 | 79 | 87.3% | -$1.01M |

| F4 | 2025-02-03 → 2025-03-31 | 80 | 71.2% | -$3.94M |

| F5 | 2025-04-01 → 2025-05-30 | 84 | 70.2% | -$5.57M |

| F6 | 2025-06-02 → 2025-07-31 | 83 | 97.6% | $1.92M |

| F7 | 2025-08-01 → 2025-09-30 | 82 | 95.1% | $1.90M |

| F8 | 2025-10-01 → 2025-11-28 | 81 | 86.4% | -$2.03M |

| F9 | 2025-12-01 → 2026-01-30 | 78 | 92.3% | $1.50M |

| F10 | 2026-02-02 → 2026-03-31 | 81 | 75.3% | -$2.35M |

| F11 | 2026-04-01 → 2026-05-11 | 56 | 85.7% | $649K |